Over $50K

Annual Revenue

Over 6 Months

Time in business

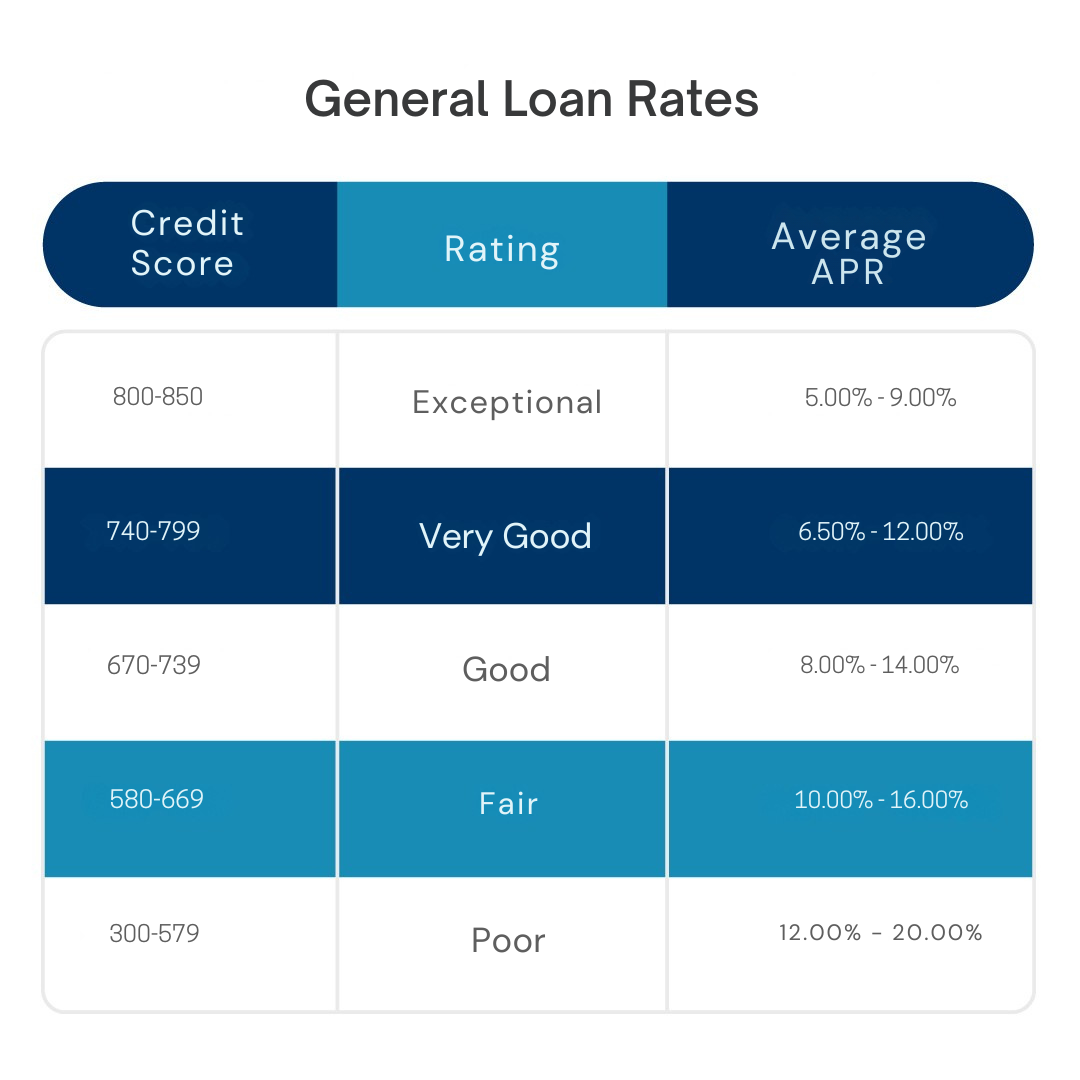

600+

Credit Score

Annual Revenue

Time in business

Credit Score

Debtors can make use of the financial process of refinancing to change a present loan for a new one with different loan terms. It is often employed in order to get a lower interest rate, lower month-to-month payment, reduced loan duration or to get a lot more money. There are different types of loans that can be refinanced, including mortgages, personal loans, auto loans, and business loans.

Refinancing is the act of acquiring a new loan, with different terms and conditions, to replace an existing loan or debt obligation. It is generally undertaken by borrowers to improve cash flow, secure cheaper interest rates, alter repayment terms or consolidate debt. Once the new loan settles the initial debt, the borrower begins paying payments in line with the new arrangement. Understanding refinancing is crucial as it assists people and organizations to manage their debt more skilfully, enhance their financial stability and potentially save large sums of money over the course of a loan. Refinancing can be advantageous if interest rates in the market have fallen or if a borrower’s financial standing has improved as it provides access to better loan terms and conditions.

Refinancing can reduce the interest costs by replacing a high cost loan with a lower interest rate. This decrease in borrowing cost allows borrowers to have more flexibility with their finances, save money over time, and allocate more of their finances toward savings, investments and other important goals.

The potential to lower monthly payments is another benefit. By arranging lower interest rates or longer loan terms, borrowers can alleviate their current financial burden.Shorter payments will improve cash flow, enabling the management of domestic spending plans and budgets.

Because of Debt Consolidation Refinancing, there is the opportunity to merge a number of debts into a single loan. This helps to make repayments easier to manage, reduces the administrative burden and helps borrowers to stay on top of their responsibilities. Consolidation can also lower the total cost of the loan, when added to the interest rate that’s available.

Financial Stability Refinancing is an increased financial stability refinance, which lets borrowers shift from variable rates to fixed rates. That means monthly payments are more predictable, with no potential rate increases down the road. The added stability does a lot to reduce uncertainty and help you plan and budget for the long term.

One of the major benefits is that of long-term cost savings. Over the course of the loan, lower interest rates lower the overall cost of borrowing. With these savings, many borrowers are now considering refinancing as an attractive option, especially for traditional homeowners who have large loans.

Refinancing can be an effective way to improve financial management by matching loan terms to current market conditions. Those with higher incomes or better credit scores may qualify for more favorable terms. This flexibility can help to ensure debt structures are appropriate and flexible to changing financial needs.

Another benefit is the option to leverage equity through special refinancing options. Residents can take advantage of the opportunity to access cash for major expenses, education or repairs.

Total interest costs are often reduced even if monthly payments are increased. Fast repayment improves financial security and allows borrowers to clear their debt faster than anticipated. Refinancing can help people to pay off their loans faster by opting for shorter loan periods. Responsible access to equity provides financial opportunities and accesses value created through owned property assets.

Refinancing often includes costs and fees which may reduce potential savings. Financial constraints could include the cost of applying, legal fees and administrative costs. Lenders should carry out a detailed analysis to establish whether the benefits outweigh the costs before refinancing.

Refinancing a loan could extend the term of the loan thus reducing monthly costs but could also increase the amount of interest paid over a period of time. Borrowers could find themselves spending more altogether despite quick increases in affordability. It is vital to understand the long-term effects before opting for lengthier repayment plans.

Standards are strict, some borrowers may have difficulty meeting the standards. Many lenders will check credit scores, stability of income, and the level of debt before approving a loan. Weaker financial profiles may make lenders less inclined or able to offer acceptance or good refinancing terms.

Market conditions may impact the Uncertain Market Conditions Refinancing results. It's possible that interest rates won't drop enough to warrant renewing an existing loan. While refinancing can be advantageous in some situations, it can also be a time, energy and cost consuming process.

Conclusion

A useful financial instrument, refinancing allows borrowers to swap out their current loans for new ones that better fit their needs. Refinancing offers a variety of opportunities to improve your finances, from reducing your interest rates to cutting your mortgage payments, consolidating debt or improving cash flow. However, a full analysis of the cost, benefit and long-term consequences is necessary to successfully refinance. Borrowers should consider what lenders want, compare the choices, and calculate their potential savings before making a decision. There are clear advantages to refinancing a house, but also disadvantages, limitations and dangers when borrowing a longer loan. This information about their pros and cons allows people and businesses to make informed choices. When done correctly, refinancing can improve overall debt management, support individual or organizational goals and enhance financial health. Ultimately, the decision to refinance is a personal one and depends on a borrower’s financial situation, market conditions and plans for the future.

Families refinance loans for many reasons to reduce borrowing costs, shorten repayment terms, consolidate loans, or improve cash flow. When market interest rates fall substantially or when borrowers’ financial circumstances improve substantially, refinancing can also help them get good terms.

Because of credit inquiries made by lenders in loan applications, refinancing can affect credit scores in the short term.

Responsible repayment of the new loan can help long-term credit development and show good financial behaviour to prospective lenders and creditors. Refinancing can actually lead to lower monthly payments through either extended payback periods or lower interest rates. While longer payback periods may result in more total interest paid by the end of the loan, lower monthly payments can enhance cash flow and financial flexibility.

No, refinancing is available for all kinds of debt, including business loans, car loans, personal loans and mortgages. The goal is the same for all types of loans to get better terms, reduce expenses or improve financial management results.

Yes, there are risks associated with refinancing, such as fees, difficulties qualifying and potentially higher total interest payments if the payback terms are extended. Borrowers should consider both the short-term advantages and the long-term impact when trying to determine if refinancing is a good choice.

Outsource Capital LLC offers a multitude of benefits for businesses in search of loans. Through our extensive network of lenders, Outsource Capital enables businesses to tap into a broader pool of financing options, simplifying the application process and facilitating access to competitive loan terms. The network’s versatility and the expertise of its lenders make it an appealing choice for businesses of all scales.

With the ever-evolving lending landscape, exploring Outsource Capital’s network of lenders can present businesses with the necessary funding solutions to flourish and achieve success.

The information provided in this article is for informational purposes only and does not constitute financial or legal advice. Each business’s financial situation is unique, and it is recommended that businesses consult with qualified financial and legal professionals before making any financial or legal decisions. The accuracy and applicability of the information provided may vary depending on individual circumstances and should not be relied upon without independent verification. The author and the publisher of this article are not responsible for any financial losses, damages, or legal consequences arising from the use or reliance upon the information provided.

You cannot copy content of this page