Over $100,000+

Annual Revenue

Over 1+ Year

Time in business

700+

Credit Score

Annual Revenue

Time in business

Credit Score

When businesses require a lump sum of capital for a specific purpose, term loans serve as a popular financing option. Unlike a line of credit loans that provide ongoing access to funds, term loans offer a fixed loan amount that is repaid over a predetermined period with regular installment payments. In this article, we will delve into the advantages, pros, and cons of term loans to help businesses understand their financing options more comprehensively.

A term loan is a type of loan that provides borrowers with a fixed amount of money upfront, which is repaid over a specified period, known as the loan term. These loans can be obtained from banks, financial institutions, or online lenders. The repayment term is predetermined and can range from a few months to several years, depending on the lender’s terms and the borrower’s creditworthiness.

Term loans can be either secured, requiring collateral, or unsecured, without the need for collateral but typically having higher interest rates. They are commonly used by businesses to finance long-term investments, such as equipment purchases, expansion projects, or real estate acquisitions. For individual borrowers, term loans can be used for larger purchases like a car, home improvement, or debt consolidation. Regular installments are made throughout the loan term, consisting of both principal and interest payments, until the loan is fully repaid.

One of the primary advantages of a term loan is the ability to secure a lump sum of capital upfront. This can be particularly beneficial for businesses with well-defined investment or expansion plans that require a substantial amount of funding at once.

Term loans come with a predetermined repayment schedule, allowing businesses to plan and budget accordingly. The fixed installment payments over the loan term provide predictability and facilitate better financial management.

Term loans often come with fixed interest rates, providing businesses with stability in their loan payments. This allows businesses to avoid the uncertainties associated with variable interest rates and can simplify financial planning.

Term loans often have more flexible payback periods. This long-term financing can be advantageous for businesses as it spreads out the repayment burden over an extended period, making it more manageable and reducing the strain on cash flow.

Term loans may offer lower interest rates compared to shorter-term or unsecured loans. Businesses with strong credit profiles and established track records may qualify for more favorable interest rates, resulting in cost savings over the loan’s duration.

Businesses that need funding for equipment, real estate, or growth might consider term loans. The availability of a lump sum allows businesses to make substantial investments and pursue growth opportunities.

Timely repayment of a term loan can help businesses build a positive credit history. Demonstrating a responsible payment record can enhance the business's creditworthiness, potentially leading to better borrowing terms and conditions in the future.

Compared to seeking equity investments, term loans allow businesses to maintain full ownership and control. With term loans, businesses do not dilute their equity or share profits with external investors, preserving their autonomy and decision-making power.

Term loan interest is often tax deductible. Businesses may profit from a lower taxable revenue and tax burden.

Unlike a line of credit loans, term loans do not offer the flexibility to borrow and repay funds as needed. Once the loan amount is disbursed, businesses are committed to making regular installment payments, regardless of their immediate financial circumstances. This rigidity may pose challenges for businesses experiencing temporary cash flow fluctuations

Term loans may require collateral to secure the loan, such as real estate, equipment, or other business assets. This collateral serves as security for the lender but can be a barrier for businesses that lack substantial assets to pledge. Failure to repay the loan may result in the loss of the pledged collateral.

Some term loans come with prepayment penalties, which are charges imposed if the loan is paid off before the agreed-upon term. These penalties can deter businesses from early repayment, even if they have the means to do so.

Term loans often have specific qualification criteria, such as minimum credit scores, business history, and financial statements. Small or new businesses may face challenges in meeting these criteria, limiting their access to term loan financing.

Conclusion

Term loans offer businesses a valuable option for accessing a lump sum of capital with predictable repayment terms. The advantages of term loans include lump sum capital, predictable repayment schedules, fixed interest rates, long-term financing options, and potentially lower interest rates. Term loans provide purpose-specific financing, help businesses build credit, preserve equity ownership, and may offer tax deductibility. However, businesses should also consider the cons, such as rigidity in repayment, collateral requirements, prepayment penalties, and qualification criteria. By carefully evaluating their financing needs and weighing the pros and cons, businesses can make informed decisions about utilizing term loans as a strategic financing tool.

A term loan is a type of financing where a business borrows a lump sum from a lender and repays it with interest over a fixed period. It’s often used for large investments like equipment, expansion, or real estate.

Term loans typically have repayment periods ranging from 1 to 10 years for short- and medium-term loans. Long-term loans, often for real estate or large capital investments, may have terms extending up to 30 years.

Businesses with a solid credit history, steady revenue, and profitability are more likely to qualify. Lenders often require financial statements, a business plan, and sometimes collateral.

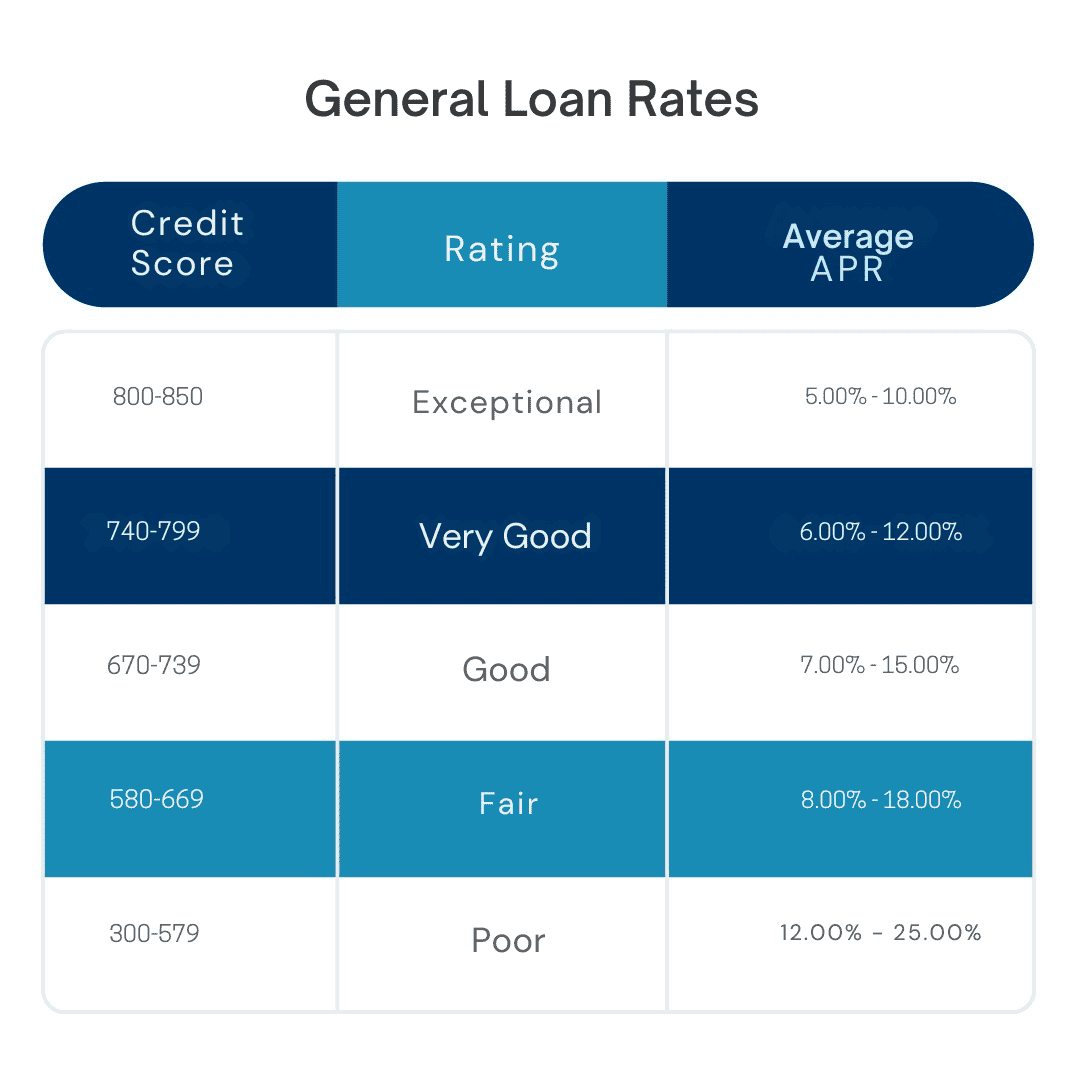

Interest rates vary based on the borrower’s creditworthiness, loan amount, and term length. Rates are generally fixed, but some lenders may offer variable rates tied to the prime rate.

Many term loans, especially larger ones, require collateral—such as real estate, equipment, or inventory—as security. If the borrower defaults, the lender may seize the collateral to recover losses.

Yes, businesses often use term loans to refinance high-interest debt. Consolidating debt with a term loan can result in lower monthly payments and reduced interest costs.

Outsource Capital LLC offers a multitude of benefits for businesses in search of loans. Through our extensive network of lenders, Outsource Capital enables businesses to tap into a broader pool of financing options, simplifying the application process and facilitating access to competitive loan terms. The network’s versatility and the expertise of its lenders make it an appealing choice for businesses of all scales.

With the ever-evolving lending landscape, exploring Outsource Capital’s network of lenders can present businesses with the necessary funding solutions to flourish and achieve success.

The information provided in this article is for informational purposes only and does not constitute financial or legal advice. Each business’s financial situation is unique, and it is recommended that businesses consult with qualified financial and legal professionals before making any financial or legal decisions. The accuracy and applicability of the information provided may vary depending on individual circumstances and should not be relied upon without independent verification. The author and the publisher of this article are not responsible for any financial losses, damages, or legal consequences arising from the use or reliance upon the information provided.

We connect businesses with a network of lenders to facilitate access to various financing options. Still, the decision to apply for a loan and the choice of lender remains solely with the user.

Outsource Capital LLC does not guarantee the accuracy, completeness, or timeliness of the information provided, nor does it guarantee the approval of any loan application or the terms of any loan offer.

You cannot copy content of this page