N/A

Annual Revenue

N/A

Time in business

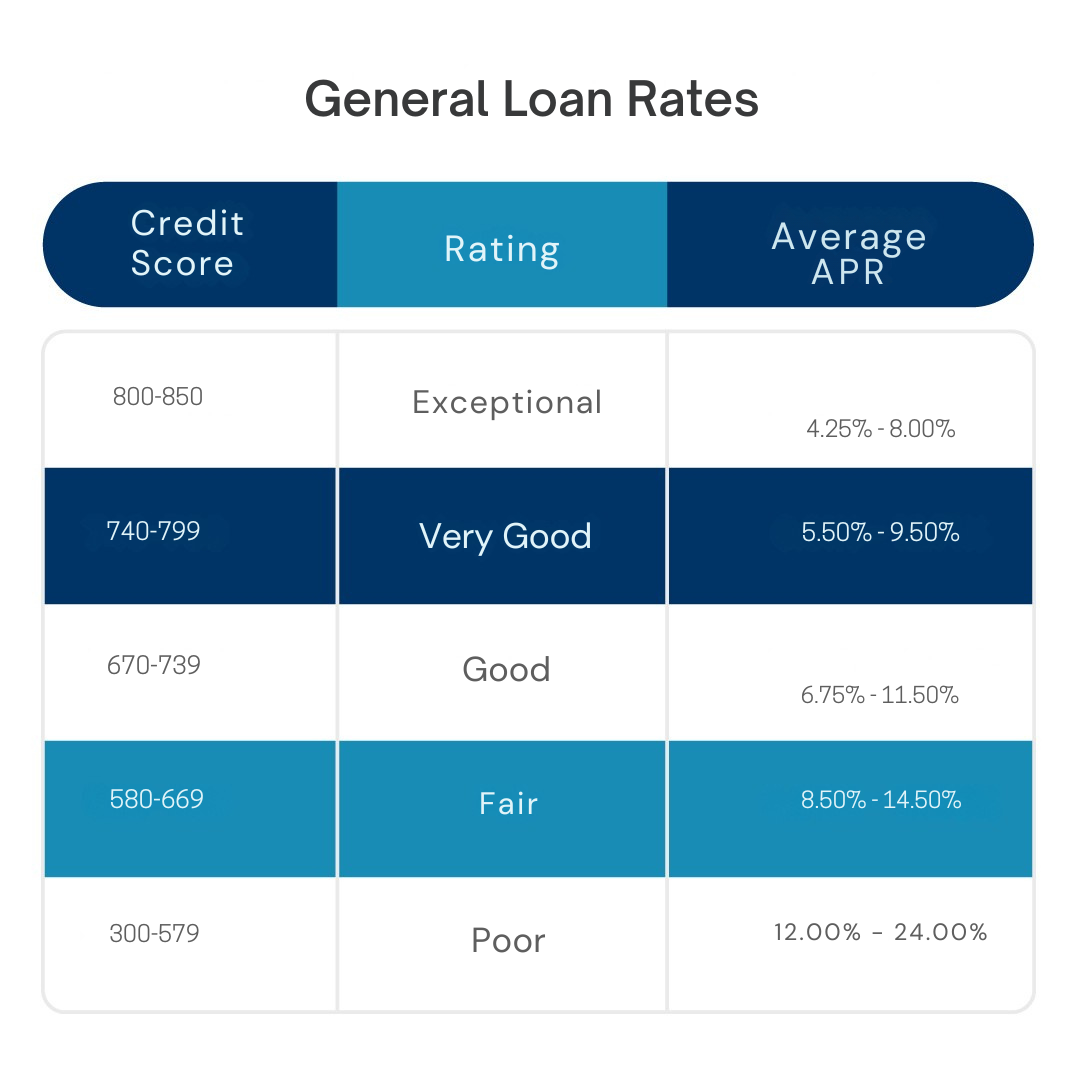

580+

Credit Score

Annual Revenue

Time in business

Credit Score

Purchasing a home is a significant milestone, but for many individuals, the financial barriers can seem insurmountable. Federal Housing Administration (FHA) loans serve as a lifeline for aspiring homeowners, especially those with limited credit history or a lower down payment. These government-backed loans provide an accessible path to homeownership, helping borrowers secure affordable financing and achieve the dream of having a place to call their own. This comprehensive exploration delves into the intricacies of FHA loans, unveiling their advantages, pros, and cons, empowering potential homebuyers with the knowledge to navigate the world of mortgage financing with informed decision-making.

FHA Loans are mortgage loans backed by the Federal Housing Administration, a government agency within the U.S. Department of Housing and Urban Development (HUD). These loans are designed to assist low-to-moderate-income borrowers and first-time homebuyers who may have difficulty meeting the down payment requirements of conventional loans. FHA Loans offer more flexible eligibility criteria and require a lower down payment, making homeownership attainable for many Americans.

FHA loans offer a lower down payment requirement compared to traditional mortgages, making homeownership more accessible.

FHA loans are often more forgiving of credit histories, enabling borrowers with lower credit scores to qualify.

FHA loans are backed by the government, reducing lender risk and enabling favorable loan terms.

Borrowers can benefit from competitive interest rates, enhancing affordability over the loan term.

FHA loans offer both fixed and adjustable-rate options, providing flexibility to suit different financial situations.

FHA loans make it possible for first-time homebuyers and individuals with limited resources to enter the housing market.

FHA loans can be assumed by qualified borrowers, potentially making the home more attractive to future buyers.

Borrowers with existing FHA loans can take advantage of streamlined refinancing options to lower interest rates or change loan terms.

FHA loans often require borrowers to receive financial counseling, promoting informed homeownership.

FHA loans can include funds for energy-efficient home improvements through the Energy Efficient Mortgage program.

Borrowers are required to pay mortgage insurance premiums, which add to the overall cost of the loan.

FHA loans have maximum loan limits, which vary by location and can impact the affordability of certain properties.

FHA loans require homes to meet certain property standards, potentially limiting options in the housing market.

The FHA loan process can involve additional documentation and requirements compared to conventional loans.

Refinancing an FHA loan into a conventional loan can be challenging due to stricter requirements.

Conclusion

FHA loans stand as a crucial avenue for individuals seeking to overcome the financial barriers to homeownership. The advantages of low down payments, flexible credit requirements, government backing, competitive rates, and flexible loan options underscore their significance.

Complementing these advantages are the pros of accessible entry, assumable loans, streamlined refinancing, financial counseling, and energy efficiency improvements. However, potential homebuyers must consider the disadvantages of mortgage insurance premiums, loan limits, property standards, the complexity of the process, and potential challenges in refinancing.

In the dynamic landscape of mortgage financing, well-informed decisions are paramount. Potential homebuyers must assess their financial readiness, research loan options, and understand the terms and conditions of FHA loans. By approaching FHA loans with strategic insight, a comprehensive understanding of both the benefits and challenges, and a commitment to responsible homeownership, individuals can confidently embark on the journey to homeownership, secure affordable financing, and lay the foundation for a stable and fulfilling future.

The minimum credit score required for an FHA Loan is typically around 580, but some lenders may accept scores as low as 500 with a higher down payment.

No, FHA Loans are intended for owner-occupied properties only, and borrowers must certify that they will occupy the property as their primary residence.

Mortgage insurance protects the lender in case the borrower defaults on the loan. The upfront and annual mortgage insurance premiums are used to fund this insurance.

Yes, FHA offers various refinancing options, including the FHA Streamline Refinance, which allows borrowers to refinance their existing FHA Loan with minimal documentation.

Yes, the seller’s contribution towards closing costs is limited to a specific percentage of the home’s purchase price, typically around 6%.

Outsource Capital LLC offers a multitude of benefits for businesses in search of loans. Through our extensive network of lenders, Outsource Capital enables businesses to tap into a broader pool of financing options, simplifying the application process and facilitating access to competitive loan terms. The network’s versatility and the expertise of its lenders make it an appealing choice for businesses of all scales.

With the ever-evolving lending landscape, exploring Outsource Capital’s network of lenders can present businesses with the necessary funding solutions to flourish and achieve success

The information provided in this article is for informational purposes only and does not constitute financial or legal advice. Every business’s financial situation is unique, and it is recommended that businesses consult with qualified financial and legal professionals before making any financial or legal decisions. The accuracy and applicability of the information provided may vary depending on individual circumstances and should not be relied upon without independent verification. The author and the publisher of this article are not responsible for any financial losses, damages, or legal consequences arising from the use or reliance upon the information provided.

We connect businesses with a network of lenders to facilitate access to various financing options. Still, the decision to apply for a loan and the choice of lender remains solely with the user.

Outsource Capital LLC does not guarantee the accuracy, completeness, or timeliness of the information provided, nor does it guarantee the approval of any loan application or the terms of any loan offer.

You cannot copy content of this page