N/A

Annual Revenue

N/A

Time in business

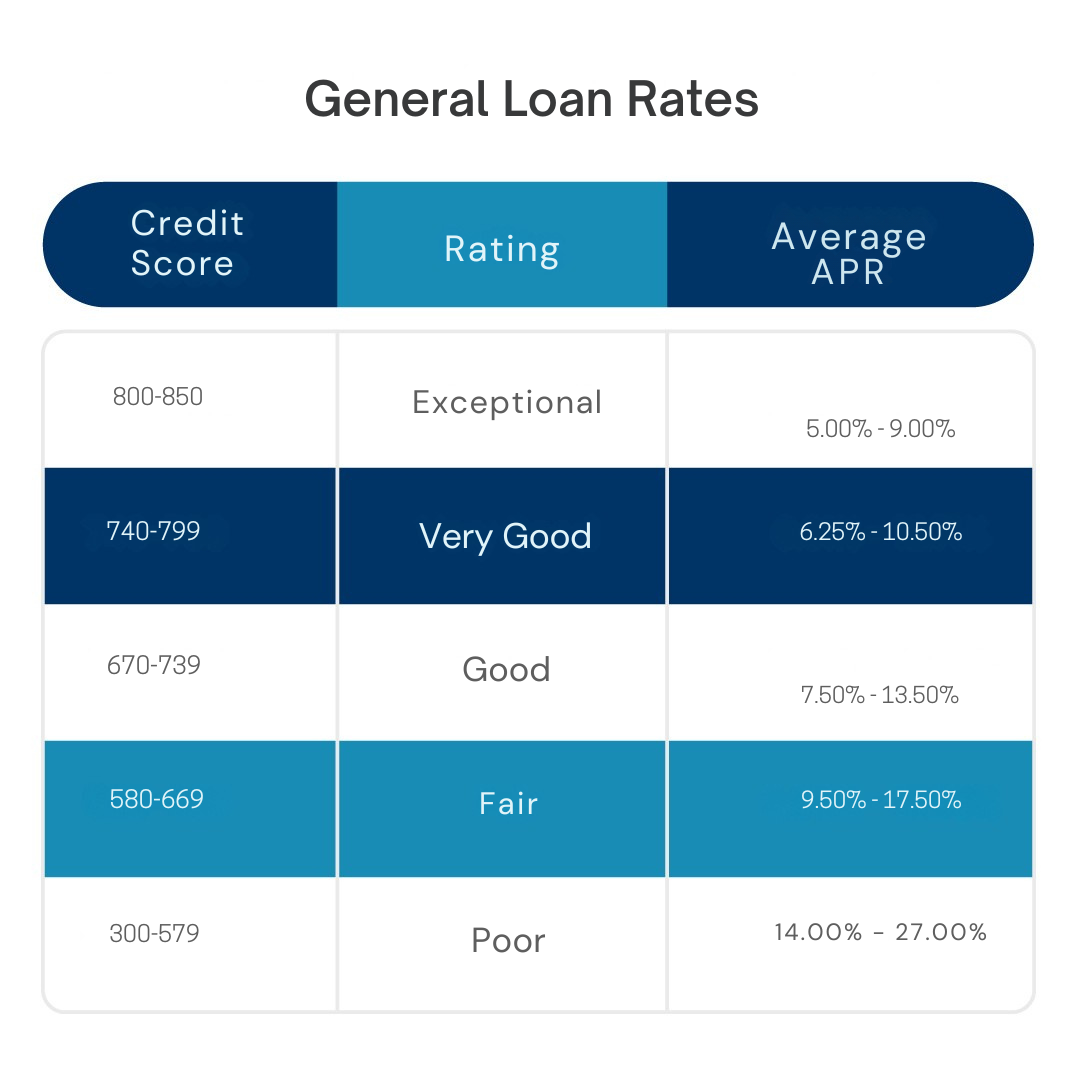

620+

Credit Score

Annual Revenue

Time in business

Credit Score

Homeownership represents a valuable asset that holds potential beyond providing shelter. Equity loans, also known as home equity loans or second mortgages, empower homeowners to unlock the value of their property for various financial needs. By using the equity built up in their homes, individuals can access funds to support home improvements, debt consolidation, education, or other expenses. This comprehensive exploration delves into the intricacies of equity loans, unveiling their advantages, pros, and cons, equipping homeowners with the knowledge to make informed decisions about their financial strategies.

An Equity Loan, also known as a home equity loan or second mortgage, is a type of loan that allows borrowers to borrow against the equity in their property. Equity refers to the difference between the property’s current market value and the outstanding mortgage balance. Equity Loans provide borrowers with a lump sum amount, typically at a fixed interest rate, which they can use for specific purposes.

Equity loans provide homeowners with a source of accessible funds based on the value of their property.

Interest rates on equity loans are often lower than rates on credit cards or personal loans.

Borrowers can utilize equity loan funds for a wide range of purposes, including home renovations, education, and debt consolidation.

In some cases, the interest paid on equity loans might be tax-deductible, reducing the overall cost.

Equity loans allow homeowners to retain ownership of their property while leveraging its value.

Many equity loans come with fixed interest rates, ensuring predictable monthly payments.

Borrowers receive a lump sum of funds upfront, which can be particularly useful for large expenses.

Equity loans typically have longer repayment terms, leading to lower monthly payments.

Fixed monthly payments simplify budgeting and financial planning.

If property values increase over time, homeowners can potentially access even more equity in the future.

Borrowers must consider the interest costs associated with equity loans, which contribute to the overall expense.

Defaulting on equity loan payments can result in the loss of the property through foreclosure.

Lenders assess creditworthiness and might require documentation similar to the process for a first mortgage.

Taking out an equity loan decreases the equity value of the property, impacting potential future sales or refinancing.

Property values can fluctuate, affecting the actual value available for borrowing.

Conclusion

Equity loans stand as a valuable financial tool for homeowners looking to utilize their property’s value for various needs. The advantages of accessible funds, lower interest rates, diverse use of funds, potential tax benefits, and preserved ownership underscore their significance.

Complementing these advantages are the pros of fixed interest rates, lump-sum access, longer repayment terms, structured repayment, and the potential for home value appreciation. However, homeowners must consider the disadvantages of interest costs, property risk, loan approval processes, reduced equity, and the impact of market fluctuations.

In the dynamic landscape of personal finance, well-informed decisions are paramount. Homeowners must evaluate their financial goals, assess their property’s equity value, and understand the terms and conditions of equity loans. By approaching equity loans with strategic planning, a comprehensive understanding of both the benefits and challenges, and a commitment to responsible borrowing, individuals can confidently leverage their property’s value, address financial needs, and enhance their overall financial well-being.

While both allow borrowing against home equity, an Equity Loan provides a lump sum amount with fixed interest rates, while a HELOC works like a credit card with a revolving credit line.

While some lenders allow using Equity Loans for investment purposes, it’s essential to carefully consider the risks and consult a financial advisor.

Failure to repay the Equity Loan could lead to default and potential foreclosure, resulting in the loss of the property.

Failure to repay the Equity Loan could lead to default and potential foreclosure, resulting in the loss of the property.

Lenders typically assess the property’s appraised value, outstanding mortgage balance, and the borrower’s creditworthiness to determine the loan amount.

Generally, borrowers have the flexibility to use the funds from an Equity Loan for various purposes, but it’s advisable to review the lender’s terms and conditions for any specific restrictions.

Outsource Capital LLC offers a multitude of benefits for businesses in search of loans. Through our extensive network of lenders, Outsource Capital enables businesses to tap into a broader pool of financing options, simplifying the application process and facilitating access to competitive loan terms. The network’s versatility and the expertise of its lenders make it an appealing choice for businesses of all scales.

With the ever-evolving lending landscape, exploring Outsource Capital’s network of lenders can present businesses with the necessary funding solutions to flourish and achieve success

The information provided in this article is for informational purposes only and does not constitute financial or legal advice. Every business’s financial situation is unique, and it is recommended that businesses consult with qualified financial and legal professionals before making any financial or legal decisions. The accuracy and applicability of the information provided may vary depending on individual circumstances and should not be relied upon without independent verification. The author and the publisher of this article are not responsible for any financial losses, damages, or legal consequences arising from the use or reliance upon the information provided.

We connect businesses with a network of lenders to facilitate access to various financing options. Still, the decision to apply for a loan and the choice of lender remains solely with the user.

Outsource Capital LLC does not guarantee the accuracy, completeness, or timeliness of the information provided, nor does it guarantee the approval of any loan application or the terms of any loan offer.

You cannot copy content of this page