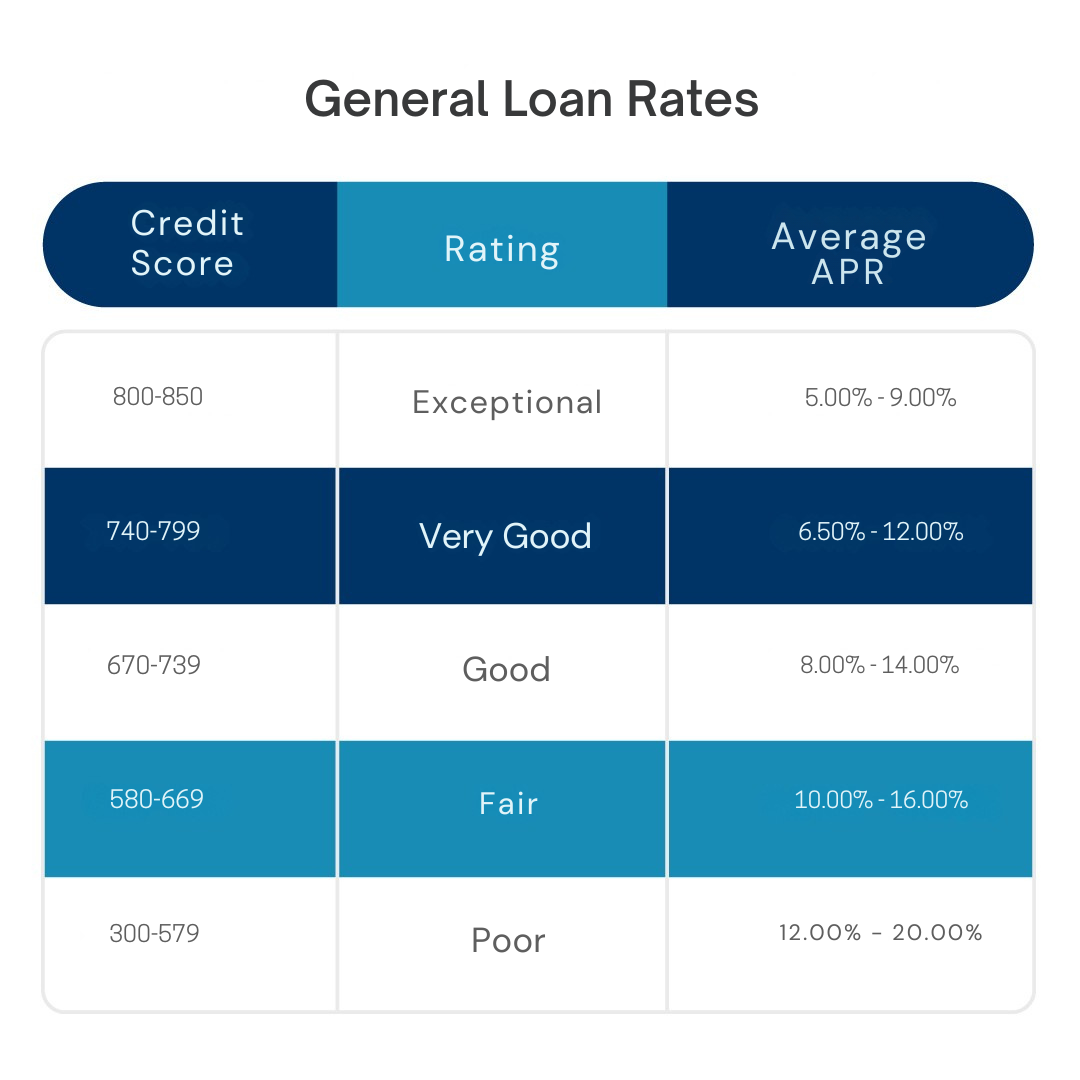

Over $50K

Annual Revenue

Over 6 Months

Time in business

600+

Credit Score

Annual Revenue

Time in business

Credit Score

Asset Based Acquisition Financing is a method of financing an acquisition when the assets of the company being sold or the company buying the company is the guarantee used to finance the purchase. These assets can be in the form of goods, receivables, equipment or property. It can be used when financing is unavailable or when the funds needed for a purchase is from another source, such as cash flow. This type of financing is crucial since it allows firms to release the value of tangible assets, enhance liquidity and enable acquisitions, whilst decreasing reliance on unsecured borrowing or equity dilution.

The loans are backed by the assets of the firm making the acquisition, or the target business being acquired. Lenders will take into consideration the value of assets like accounts receivable, inventory, machinery and real estate to determine how much they can lend. The amount of the loan is often a proportion of the value of the asset (the advance rate). This is a frequent method of financing for mergers and acquisitions, especially for those organizations with solid asset bases but lower cash flows. It backs acquisitions and provides a collateral backstop to lenders. It’s a structured and secured type of purchase financing that can be taken and sold by the lenders in the case of the borrower’s default.

Organizations can borrow massive amounts of capital based on the value of their assets with the use of asset based finance. Companies with larger receivables or stock might secure higher loans than those which can be obtained in an unsecured loan. This helps build acquisition capacity and enables firms to go for bigger transactions without having to depend on equity capital too much.

The financing method allows turning illiquid assets into useful capital and increasing the liquidity. This enables firms to obtain the cash that they require for acquisitions much faster than waiting for their income to grow over the long term. This ensures that transactions can be executed quickly and competition can be achieved in fast-paced acquisition markets.

The lender has less risk if the loan is secured to some real asset than if it is not secured. This can make it easier for the consumers that have less good credit histories to get funding. The versatility of collateral across asset classes increases the chances of loan acceptance and can lead to more complex loan agreements.

Asset based finance may be organized in a variety of asset categories such as inventories, equipment and receivables. This flexibility allows organizations to optimize their borrowing base upon the assets that they have on hand. It also helps to guarantee a better use of balance sheet resources to fund acquisitions.

When cash flow is unstable, companies with substantial assets can take out a loan. This decreases the barrier for mid-sized and troubled organizations to be involved in acquiring. The attention to collateral, not profitability, expands the choice of funding possibilities.

The funding is best for fast growing, or in times of stress, companies. Lending is asset-backed, so businesses don't have to have a low profit margin in order to qualify. This enables organizations to expand or restructure by using strategic acquisitions.

The asset based finance could be processed relatively quickly once the asset appraisal is complete. This is crucial to a quick acquisition in a competitive environment where time is of the essence. Having quicker access to capital boosts the efficiency of transaction execution and strategic positioning.

Purchase finance is not the only use for asset based loans; they can also be used to provide working capital. “The double effect will ensure that companies both will be able to complete acquisitions and continue to operate well post-transaction.

Lenders secure assets of the firm to which the assets are attached, where the assets can be taken if the firm does not pay. This poses a huge danger to the continuation of operations - especially if collateralized with critical assets like machinery or inventories.

The value of assets available limits the borrowing ability. Not suitable for companies that are asset light like service companies, technology companies that may not have or depreciating assets and may not meet the finance criteria.

Lenders will often want periodic review and evaluation of the collateral offered. These demands create administrative pressures, compliance costs, lack of flexibility in operations and increase the complexity of financial management for organizations.

The Asset based financing involves a lot of asset audits, legal documentation and appraisal procedures. These regulations could lead to increased transaction costs and potentially lengthened acquisition timelines, particularly for complex or multi-asset acquisitions.

Conclusion

Asset based acquisition financing is an essential fundraising instrument. It helps organizations to obtain funds by leveraging the value of their physical and financial assets. This is a different approach to conventional finance techniques and especially relevant for those organizations that don’t generate large cash flows but do have valuable assets. This form of finance facilitates acquisitions by enhancing liquidity, boosting borrowing capacity and allowing faster transaction execution. But it also presents concerns of asset confiscation in case of default, limited borrowing based on asset valuation and more stringent compliance standards. There are downsides but it’s still a common option for mid-sized corporations, troubled companies and asset-heavy sectors. It’s pretty safe for lenders because to the need for collateral, yet it still offers borrowers freedom. Properly structured asset based acquisition finance can provide sustainable development and strategic expansion without equity dilution. Ultimately, its success depends on right asset assessment, sound financial planning and prudent debt management. This creates a strong link between asset strength and acquisition opportunity, allowing organizations to transform current assets into growth capital in competitive financial markets.

Common assets are accounts receivable, inventories, machinery, equipment and real estate. Lenders assess these assets to establish the limitations of lending and the loan-to-value ratios for funding acquisitions.

It is also widely used by retail companies, manufacturing companies, troubled companies with good asset bases but poor cash flows, and mid-sized companies.

The amount of the loan is a percentage of the value of the asset, called the advance rate. Assets of greater quality tend to provide you the ability to borrow more money.

Once the assets are evaluated and validated, it may be rather quick. But due diligence and legal procedures may still take some time depending on the intricacy of the deal.

If the firm fails on the loan , then the lender can take the assets and sell them so they can get their loan back . This makes it less of a risk for the lender.

Outsource Capital LLC offers a multitude of benefits for businesses in search of loans. Through our extensive network of lenders, Outsource Capital enables businesses to tap into a broader pool of financing options, simplifying the application process and facilitating access to competitive loan terms. The network’s versatility and the expertise of its lenders make it an appealing choice for businesses of all scales.

With the ever-evolving lending landscape, exploring Outsource Capital’s network of lenders can present businesses with the necessary funding solutions to flourish and achieve success.

The information provided in this article is for informational purposes only and does not constitute financial or legal advice. Each business’s financial situation is unique, and it is recommended that businesses consult with qualified financial and legal professionals before making any financial or legal decisions. The accuracy and applicability of the information provided may vary depending on individual circumstances and should not be relied upon without independent verification. The author and the publisher of this article are not responsible for any financial losses, damages, or legal consequences arising from the use or reliance upon the information provided.

You cannot copy content of this page