For those who assume dwelling costs are too costly, you wouldn’t be the one one.

A brand new evaluation from First American revealed that housing affordability is the bottom it has been in additional than three a long time.

In different phrases, it hasn’t been this costly to buy a house because the twentieth century.

The title and settlement firm’s Actual Home Value Index (RHPI) determines house-buying energy utilizing median family revenue, mortgage charges, and residential costs.

They usually discovered that actual home costs, adjusted for these components, had been up practically 17 % year-over-year in July.

Blame Greater Mortgage Charges and Dwelling Costs for a Lack of Affordability

As for why housing affordability continues to erode, it’s a mix of things.

The primary and most evident situation is markedly greater mortgage charges, with the 30-year fastened mortgage now priced above 7%, assuming low cost factors aren’t paid.

Per Freddie Mac, charges on this most-popular mortgage program are up about 1% from year-ago ranges. First American pegs the annual change at the next 1.4 share level enhance.

And if we zoom out a bit extra, this key rate of interest was within the 3% vary to start out out 2022.

So rates of interest alone have wreaked havoc on housing affordability and residential shopping for energy.

Simply take into account a mortgage quantity of $400,000 at a 3% charge versus 7% charge. We’re speaking a couple of month-to-month principal and curiosity cost of $1,686 vs. $2,661.

That’s practically $1,000 primarily based on the rate of interest enhance alone. Then it’s a must to think about greater property taxes, greater insurance coverage premiums, and so forth because of the next buy worth.

Sure, regardless of greater rates of interest, nominal dwelling costs have additionally risen year-over-year.

Whereas folks logically assume there’s an inverse relationship with dwelling costs and mortgage charges, this isn’t all the time true.

Per First American, nominal dwelling costs (not adjusted for inflation) had been additionally up 4% year-over-year.

This implies a potential dwelling purchaser faces each the next buy worth and a considerably greater mortgage charge.

And although family revenue elevated 3.7% since July 2022, it wasn’t sufficient to offset the upper prices related to the bounce in charges and rising nominal dwelling costs.

Actual Dwelling Costs Are Now Above the 2006 Peak

For those who recall the yr 2006, you may do not forget that dwelling costs peaked after which started to fall.

Again then, unsustainable dwelling worth beneficial properties had been fueled by unique financing.

Many dwelling loans had been underwritten by way of said revenue or no documentation in any respect, whereas the merchandise supplied might have been possibility ARMs and different adjustable-rate mortgages.

Moreover, the everyday down cost was at or near zero, whereas the loan-to-value (LTV) ratio was usually 100% when it concerned a mortgage refinance.

In different phrases, dwelling costs had been too excessive, debtors had little to no pores and skin within the sport, and lots of weren’t even certified to be householders.

With out the widespread use of free underwriting, dwelling costs wouldn’t have been capable of proceed rising as excessive as they did.

As we all know, the housing bubble burst set off the Nice Recession, resulting in double-digit dwelling declines and scores of brief gross sales and foreclosures.

At this time, unadjusted dwelling costs are 53.7% above these in the course of the peak in 2006, whereas actual costs are 0.7% greater than that housing growth peak.

Whereas this may be motive to fret, take into account the brand new mortgage guidelines that had been born out of that disaster.

The Means-to-Repay/Certified Mortgage Rule (ATR/QM Rule) basically outlawed a lot of what I simply talked about.

Debtors in the present day should be absolutely certified when taking out a mortgage, and the overwhelming majority are going with a 30-year fixed-rate mortgage.

Gone are the times of said revenue underwriting and detrimental amortization. That makes the present scenario extra of an affordability disaster than a housing bubble.

It’s pushed extra by a scarcity of provide than it’s free financing, with not sufficient stock to satisfy demand.

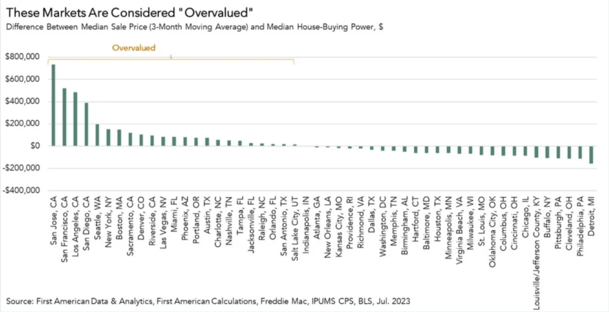

Housing Is Overvalued Nationally, However Some Markets Stay Inexpensive

As famous, the July 2023 Actual Home Value Index (RHPI) elevated about 17% from a yr in the past.

This meant the median sale worth was roughly $345,000, whereas the median house-buying energy was simply $337,000.

Since house-buying energy is under the median worth, it means housing is overvalued. In a really perfect world, it needs to be at or under the median.

Nonetheless, that applies to the nationwide median worth of actual property. Solely 24 of the 50 high markets tracked by First American are overvalued by this measure.

Granted, it has worsened over time, as solely 15 markets had been thought-about overvalued final July.

In the intervening time, San Jose, California is probably the most overvalued metro, with the median sale worth practically $1,440,000 and client house-buying energy simply $700,000.

San Francisco and Los Angeles had been additionally fairly overvalued by this measure, although to a lesser diploma.

In the meantime, some undervalued markets nonetheless exist, should you can consider it. The metros of Detroit, Philadelphia, and Cleveland are undervalued by roughly $126,000.

How Do We Repair the Unaffordable Housing Market?

We all know dwelling costs are out of attain for a lot of, however how will we repair it? Properly, the Actual Home Value Index (RHPI) takes into consideration dwelling costs, mortgage charges, and incomes.

So if you would like housing to be extra inexpensive, you want aid by way of these three components.

This implies both mortgage charges must fall, dwelling costs have to come back down, or incomes should enhance.

Otherwise you get some mixture of the three, reminiscent of a 1% drop in mortgage charges and a pullback in costs, which boosts affordability.

The issue in the meanwhile is mortgage charges may be greater for longer, and residential costs are fairly sticky as a result of a significant lack of stock (why are there no houses on the market?).

Incomes additionally don’t look to be growing by a cloth quantity, making it troublesome for potential consumers to get within the door.

One exception is new dwelling gross sales, which have relied closely on short-term and everlasting mortgage charge buydowns to deal with the financing piece.

However there are solely so many new houses on the market, and such gross sales solely usually account for 10% of the general market.

This explains the present housing market dynamic. Finally, there aren’t many present houses in the marketplace, not a ton of demand, and never a whole lot of gross sales.

And till one thing modifications, this may doubtless be the established order.

Learn extra: Why are dwelling costs so excessive proper now?

{kind=link}