Mortgage charge Q&A: “Why are mortgage charges completely different?”

Why is the sky blue? Why are clouds white? Why gained’t your neighbor trim their tree branches?

These are all good questions, and ones that always puzzle even essentially the most savvy of human beings.

First issues first, check out how mortgage charges are decided to higher perceive how banks and mortgage lenders provide you with rates of interest to start with.

From there, you’ll want to contemplate why mortgage charges are completely different for client A vs. client B, and from lender to lender.

No One Measurement Suits All for Mortgage Charges

Mortgages are sort of like snowflakes in that no two are precisely the identical (OK, probably not)The topic property and the borrower will all the time have considerably distinctive characteristicsThis means the chance on the underlying mortgage will fluctuate and so too will the rate of interest receivedLenders additionally value their mortgages in a different way so even similar eventualities can lead to variable pricing

Mortgages are sophisticated enterprise, and there definitely isn’t a one-size-fits-all method on this trade.

First off, there are literally thousands of completely different banks, lenders, and credit score unions that provide residence loans, a few of them solely distinctive and proprietary.

These firms compete with each other to supply the bottom charge and/or the very best customer support.

The well-known names would possibly provide greater charges in alternate for his or her perceived belief and familiarity.

In the meantime, the smaller guys would possibly provide rock-bottom charges to easily keep in rivalry with the massive gamers.

An enormous promoting price range would possibly imply a better charge to cowl these prices. Whereas a reduction lender would possibly be capable to cross alongside financial savings in the event that they run ultra-lean.

Together with that, each mortgage situation is completely different (similar to a snowflake), and have to be priced accordingly to think about mortgage default danger (risk-based pricing).

Merely put, the upper the chance of default, the upper the mortgage charge. However that’s simply the tip of the iceberg.

There additionally promotional charges, reminiscent of mortgage charges that finish in .99%, and modern advertising merchandise like UWM’s Precise Price that lets brokers provide unusual charge mixtures, together with 2.541% or 2.873%.

So the probabilities really are countless as of late in terms of completely different mortgage charges.

Mortgage Charges Differ Primarily based on the Mortgage Standards

Mortgage lenders make plenty of assumptions when promoting ratesYour explicit mortgage situation could also be fairly completely different than their hypothetical loanYou must bear in mind the numerous pricing changes relevant to your mortgage if it doesn’t match inside that boxThese changes have the potential to vastly enhance or lower your rate of interest

Mortgage charges don’t exist in a bubble – the components have an effect on the entire.

Banks and lenders begin with a base rate of interest (par charge) after which both elevate it or decrease it (not often) primarily based on the house mortgage’s standards.

There are mortgage pricing changes for all sorts of stuff, together with:

· Mortgage quantity (conforming or jumbo)· Documentation (full, acknowledged, and so forth.)· Credit score rating· Occupancy (main, trip, funding)· Mortgage Function (buy or refinance)· Debt-to-Earnings Ratio· Property Sort (single-family residence, condominium, multi-unit)· Mortgage-to-value / Mixed loan-to-value

The extra you’ve “obtained happening,” the upper your mortgage charge will probably be. And vice versa.

Briefly, a person buying a single-family residence with a conforming mortgage quantity, 20% down fee, and a 800 FICO rating will seemingly qualify for the bottom mortgage charges obtainable.

Conversely, the person requesting money out on a four-unit funding property with a 640 FICO rating will probably be topic to a a lot greater charge, assuming they even qualify.

I’ve already lined a couple of associated matters, together with why mortgage charges charges are greater for condos and funding properties.

Mortgage charges additionally are typically greater on jumbo loans and refinance transactions, particularly these involving cash-out.

And once more, charges will fluctuate from lender to lender, even with the identical attributes, so it’s a multi-layered scenario.

Marketed Mortgage Charges Are Finest Case Situation

Mortgage charges on TV and on-line are often best-case scenarioThey are supposed to be tremendous engaging to lure you in and snag your businessWhen the mud settles your rate of interest would possibly look nothing like what you noticed advertisedThis is why it’s necessary to buy round and higher perceive how dangerous your explicit mortgage is

these mortgage charges you see on TV or on the Web?

These assume you’ve obtained an owner-occupied single household residence, an ideal credit score rating, an enormous down fee, and a conforming mortgage quantity.

To not point out a new child golden retriever with an unmatched pedigree.

Most individuals don’t have all these issues, and consequently, they’ll see completely different mortgage charges. And by “completely different,” I principally imply greater.

How a lot greater will depend on all of the components listed above. So take the marketed charges you see with an enormous grain of salt.

Additionally, put within the time to buy your private home mortgage with completely different lenders, and within the course of, get to higher perceive your danger.

Discover out what lenders are docking you for and take steps to repair these issues if you would like the bottom charges obtainable.

Tip: Decide if you happen to can construction your mortgage barely in a different way to acquire higher pricing. This would possibly imply a better down fee or a special mortgage program, reminiscent of FHA vs. typical.

The Similar Precise Mortgage Can Be Priced In another way with Two Lenders

Now let’s assume you and one other borrower have the identical actual mortgage situation.

You’re each placing down 20% on a single-family residence buy you propose to occupy. You each have 800 FICO scores. You each need a 30-year mounted mortgage.

Heck, you’re each paying one low cost level at closing to get a barely decrease rate of interest. And for enjoyable, even the lender charges are the identical.

However someway, one lender is charging an rate of interest .50% greater than the opposite. How can that be?

Nicely, like some other enterprise, it’s good old school advertising.

Once you go to the grocery retailer, you would possibly examine two related merchandise. They each appear to be the identical, aside from the packaging. Oh yeah, and the worth.

A house mortgage might be no completely different. On the finish of the day, you’re nonetheless getting a 30-year mounted mortgage with the identical actual charge and shutting prices.

The one distinction may be the method and the customer support. However what’s extra necessary, the method or the month-to-month fee for the subsequent 30 years?

A current evaluation by the Client Monetary Safety Bureau (CFPB) discovered that value dispersion for mortgages is commonly .50% of the APR.

So it wouldn’t be unusual to see one lender promoting an APR of 6%, whereas one other presents 6.5%. For a similar actual mortgage.

In different phrases, lender alternative issues an terrible lot too, no matter your mortgage situation, mortgage sort, FICO rating, and so forth.

You won’t be capable to management your credit score rating or down fee, however you may have the power to buy round and get greater than a single quote. And it may possibly make an actual distinction!

Do Mortgage Charges Differ By State?

Sure, they certain can! You would possibly get a decrease charge in California vs. NebraskaDepending on lender urge for food for a sure geographic regionRates could fluctuate from state to state, and even in sure countiesMake certain the lender you employ presents the very best pricing for the state wherein you reside

One very last thing. I’ve been requested if mortgage charges can fluctuate from state to state, and the reply is definitely YES. The truth is, they’ll even fluctuate by county in some instances.

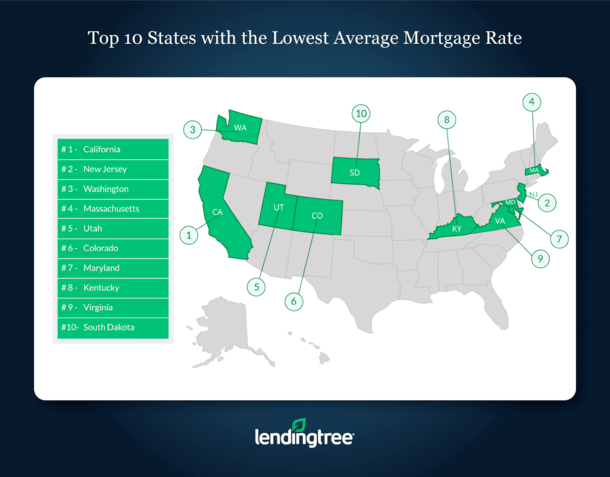

As you may see from the picture under, some states are inclined to have decrease common mortgage charges for one motive or one other.

This checklist is from February 2019, when the typical charge for the 30-year mounted was 4.84% nationwide, per LendingTree.

Whereas no state provided a median charge under 4.74% or above 4.96% (fairly slim vary), there was some divergence by locality.

California led the nation with a median charge of 4.74%, adopted carefully by the 4.75% common seen in New Jersey and the 4.76% common present in each Washington and Massachusetts.

Nothing earth-shattering, however nonetheless completely different nonetheless.

However it won’t be for anybody motive, reminiscent of a better default charge in state X or fewer pure disasters in state Y. Or extra laws in one other state.

It may very well be extra to do with the truth that lenders wish to enhance their enterprise in a sure a part of the nation, and thus they’ll provide some form of pricing particular or incentive to drive charges down in say California.

So that you would possibly see a charge sheet that claims .50% rebate state adjustment for loans in CA and FL, for instance. This may give them a aggressive benefit in these areas.

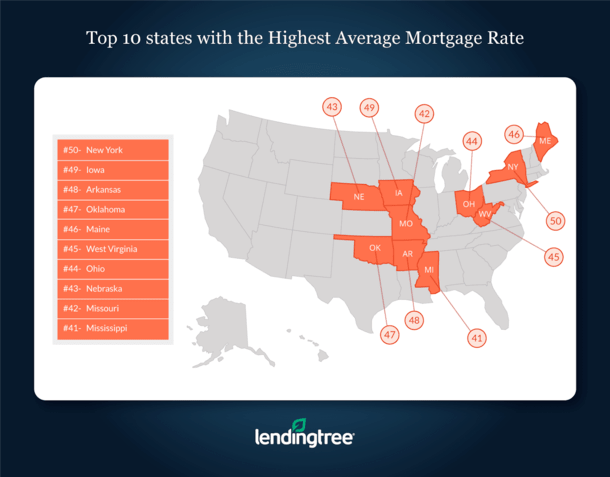

How about states the place mortgage charges are typically barely greater, reminiscent of New York, Iowa, and Arkansas, which averaged 4.96%, 4.93%, and 4.92%, respectively?

It’s attainable you would possibly see a pricing adjustment of say .25% for considered one of these states which will drive the rate of interest up considerably.

In different phrases, charges might be priced each greater or decrease relying on the state the place the property is positioned.

In fact, if this leads to unfavorable pricing you may simply transfer on to a special lender that doesn’t cost extra for the state in query.

All of the extra motive to buy round, examine mortgage charges on-line, and converse with a mortgage dealer or two.

When you’ve finished that, verify mortgage charges along with your native financial institution or credit score union as effectively.

Don’t be one of many many who receive only one mortgage quote as a result of chances are you’ll wind up paying an excessive amount of.

Learn extra: What mortgage charge can I count on?

-1.png#keepProtocol "Personal Finance for Single People")

{kind=link}