No Requirement

Annual Revenue

Over 1 month

Time in business

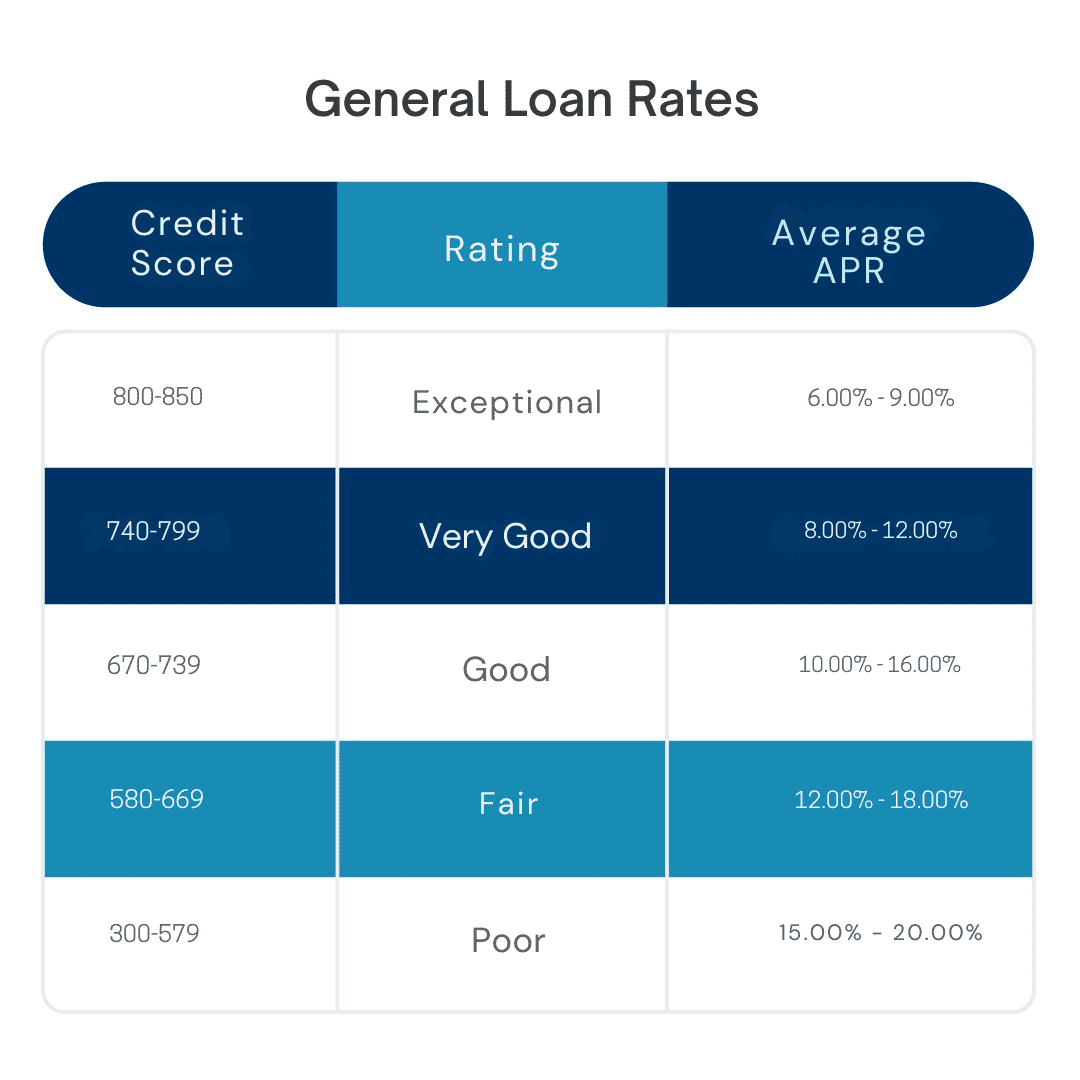

600

Credit Score

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book.Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book.

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book.Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book.

Annual Revenue

Time in business

Credit Score

Microloans are small-scale loans typically offered to individuals or small businesses with limited access to traditional financing options. These loans may boost entrepreneurship, economic growth, and financial access in underserved areas. One tool can achieve these goals. This post will explain microloans and their pros and cons for your company.

A microloan is typically of a low amount, provided to entrepreneurs, small business owners, or individuals who lack access to traditional banking services. Microloans are often used to start or expand small businesses, purchase equipment, or cover operating expenses. These loans are typically offered by microfinance institutions (MFIs) or non-profit organizations and are designed to support individuals and businesses in low-income or developing regions. Microloans aim to promote financial inclusion and economic empowerment by providing access to capital for those who may not qualify for larger bank loans

Microloans may help people and companies get cash even if they don’t qualify for traditional loans. Thus, microloans are becoming more prevalent in current society. Microloans bridge the funding gap and allow entrepreneurs to launch or expand their businesses, supporting economic development and job creation.

Microloan programs often have simplified application processes compared to traditional loans, making them more accessible to individuals or businesses with limited financial resources or credit history. The focus is typically on evaluating the borrower’s character, business plan, and ability to repay the loan rather than solely relying on credit scores or collateral.

Microloan programs often have simplified application processes compared to traditional loans, making them more accessible to individuals or businesses with limited financial resources or credit history. The focus is typically on evaluating the borrower’s character, business plan, and ability to repay the loan rather than solely relying on credit scores or collateral.

Microloan programs may offer additional support beyond the capital, such as training, mentoring, and business development resources. This holistic approach helps borrowers improve their entrepreneurial abilities, company operations, and chances of long-term success.

Microloans are particularly beneficial for start-up businesses or those in the early stages of growth. They provide the necessary funds to launch operations, purchase equipment or inventory, and cover initial expenses. Additionally, microloans can support the expansion plans of small businesses, allowing them to seize opportunities and increase their market presence.

Microloan lenders often develop personalized relationships with borrowers, offering guidance and support throughout the loan term. This close connection enhances trust and fosters a collaborative environment, leading to a deeper understanding of the borrower's needs and increasing the likelihood of successful loan repayment.

Successfully repaying a microloan can have a positive impact on the borrower's credit history. Timely payments and responsible financial management demonstrate creditworthiness and can improve the borrower's chances of qualifying for larger loans with more favorable terms in the future.

Microloans contribute to the development of local economies and communities. By supporting small businesses, microloans help create employment opportunities, stimulate economic growth, and foster entrepreneurship within underserved areas.

Microloans have far higher interest rates than bank loans. Microloans have increased administrative expenses and risk. Borrowers must evaluate the loan's entire cost and if the potential advantages merit a higher interest rate before taking it out.

While microloans provide access to capital, the loan amounts are typically limited. This may restrict the borrower's ability to undertake larger projects or significant business expansions that require substantial financial resources.

Microloans often have shorter repayment terms compared to traditional loans, requiring borrowers to make frequent and potentially higher monthly payments. This may impede a small company's cash flow, especially in its early stages when sales may be limited.

Microloans may not be universally available or easily accessible in all regions. The availability of microloan programs can vary depending on the geographic location and the specific requirements and criteria set by lenders or organizations offering microfinance services.

Conclusion

Microloans provide a valuable financing option for individuals and small businesses, offering access to capital, flexible loan amounts, simplified application processes, and non-financial support. Pros of microloans include start-up and expansion support, personalized relationships, credit-building opportunities, and positive community impact. However, it is important to consider the cons, such as higher interest rates, limited loan amounts, repayment requirements, and potential availability and accessibility limitations. If they first analyze their financial needs, then research the terms and conditions of various microloan programs, and finally consider the many alternative financing options, individuals and organizations can form informed opinions about using micro-loans as a strategic tool for their business operations.

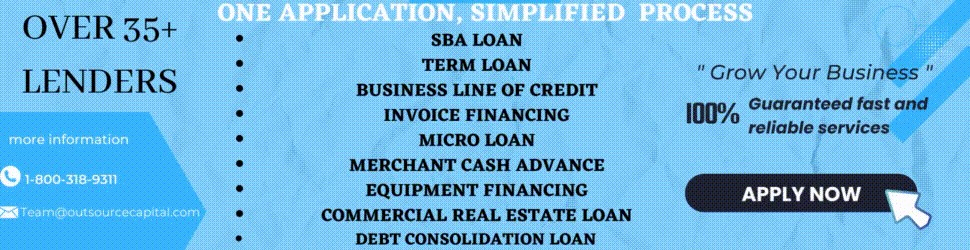

Outsource Capital LLC offers a multitude of benefits for businesses in search of loans. Through our extensive network of lenders, Outsource Capital enables businesses to tap into a broader pool of financing options, simplifying the application process and facilitating access to competitive loan terms. The network’s versatility and the expertise of its lenders make it an appealing choice for businesses of all scales.

With the ever-evolving lending landscape, exploring Outsource Capital’s network of lenders can present businesses with the necessary funding solutions to flourish and achieve success.

The information provided in this article is for informational purposes only and does not constitute financial or legal advice. Each individual or business’s financial situation is unique, and it is recommended to consult with qualified financial and legal professionals before making any financial or legal decisions. The accuracy and applicability of the information provided may vary depending on individual circumstances and should not be relied upon without independent verification. The author and the publisher of this article are not responsible for any financial losses, damages, or legal consequences arising from the use or reliance upon the information provided.

Copyright © 2023 Outsource Capital.

Outsource Capital is not responsible for the content of external sites.

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book.Copyright © 2023 Outsource Capital.

Outsource Capital is not responsible for the content of external sites.